Mar 14, 2025

BusinessKYC and AML compliance: a complete guide for businesses

KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements affect businesses across industries. Learn what these regulations require and how to build compliant verification processes.

If your business handles customer funds, provides financial services, or operates in regulated industries, you're likely subject to KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements. These regulations require businesses to verify who their customers are and monitor for suspicious activity that might indicate financial crime.

Non-compliance carries serious consequences: substantial fines, loss of operating licenses, reputational damage, and personal liability for executives. But compliance isn't just about avoiding penalties. Effective KYC and AML programs protect businesses from fraud, reduce exposure to criminal enterprises, and build customer trust.

Understanding KYC requirements

KYC refers to the process of verifying customer identity and assessing potential risks. At its core, KYC answers three questions: Who is this person? Are they who they claim to be? And what risk do they present?

Customer Identification Program (CIP): The foundation of KYC. Businesses must collect identifying information (name, date of birth, address, identification number) and verify this information through reliable documents or data sources.

Customer Due Diligence (CDD): Beyond basic identification, CDD requires understanding the nature of customer relationships. What services will they use? What transaction patterns should be expected? This information helps detect unusual activity later.

Enhanced Due Diligence (EDD): Higher-risk customers require additional scrutiny. This might include politically exposed persons (PEPs), customers from high-risk jurisdictions, or those with complex ownership structures. EDD involves deeper investigation and ongoing monitoring.

AML framework essentials

AML regulations focus on detecting and preventing money laundering: the process of making illegally obtained money appear legitimate. An effective AML program includes several components:

Transaction monitoring: Systems that flag unusual transaction patterns, such as large cash deposits, rapid movement of funds, or transactions with high-risk jurisdictions.

Suspicious Activity Reports (SARs): When suspicious activity is detected, businesses must file reports with relevant authorities. In the US, this means the Financial Crimes Enforcement Network (FinCEN). Other jurisdictions have equivalent reporting requirements.

Sanctions screening: Checking customers and transactions against sanctions lists maintained by bodies like OFAC (US), the EU, and the UN. Doing business with sanctioned entities carries severe penalties.

Record keeping: Maintaining records of customer identification, transactions, and compliance activities. Requirements vary by jurisdiction but typically span five to seven years.

Regulatory landscape by region

KYC and AML requirements vary significantly across jurisdictions. Here's an overview of major frameworks:

European Union: The Anti-Money Laundering Directives (AMLD) establish requirements across member states. The 6th AMLD expanded the definition of money laundering offenses and increased penalties. The EU is also moving toward a single AML rulebook with a new European AML Authority.

United Kingdom: The Money Laundering Regulations (MLR) implement EU directives while adding UK-specific requirements. Post-Brexit, the UK maintains equivalent standards while developing independent regulatory approaches.

United States: The Bank Secrecy Act (BSA) and USA PATRIOT Act establish AML requirements. FinCEN provides guidance and receives suspicious activity reports. Recent updates have expanded requirements to include beneficial ownership reporting.

Canada: FINTRAC (Financial Transactions and Reports Analysis Centre) administers AML requirements under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act.

Asia-Pacific: Requirements vary significantly. Singapore and Hong Kong maintain robust regimes. Australia's AUSTRAC oversees AML compliance. Many jurisdictions are strengthening requirements to meet FATF standards.

Building a compliant verification process

Effective KYC combines several verification methods:

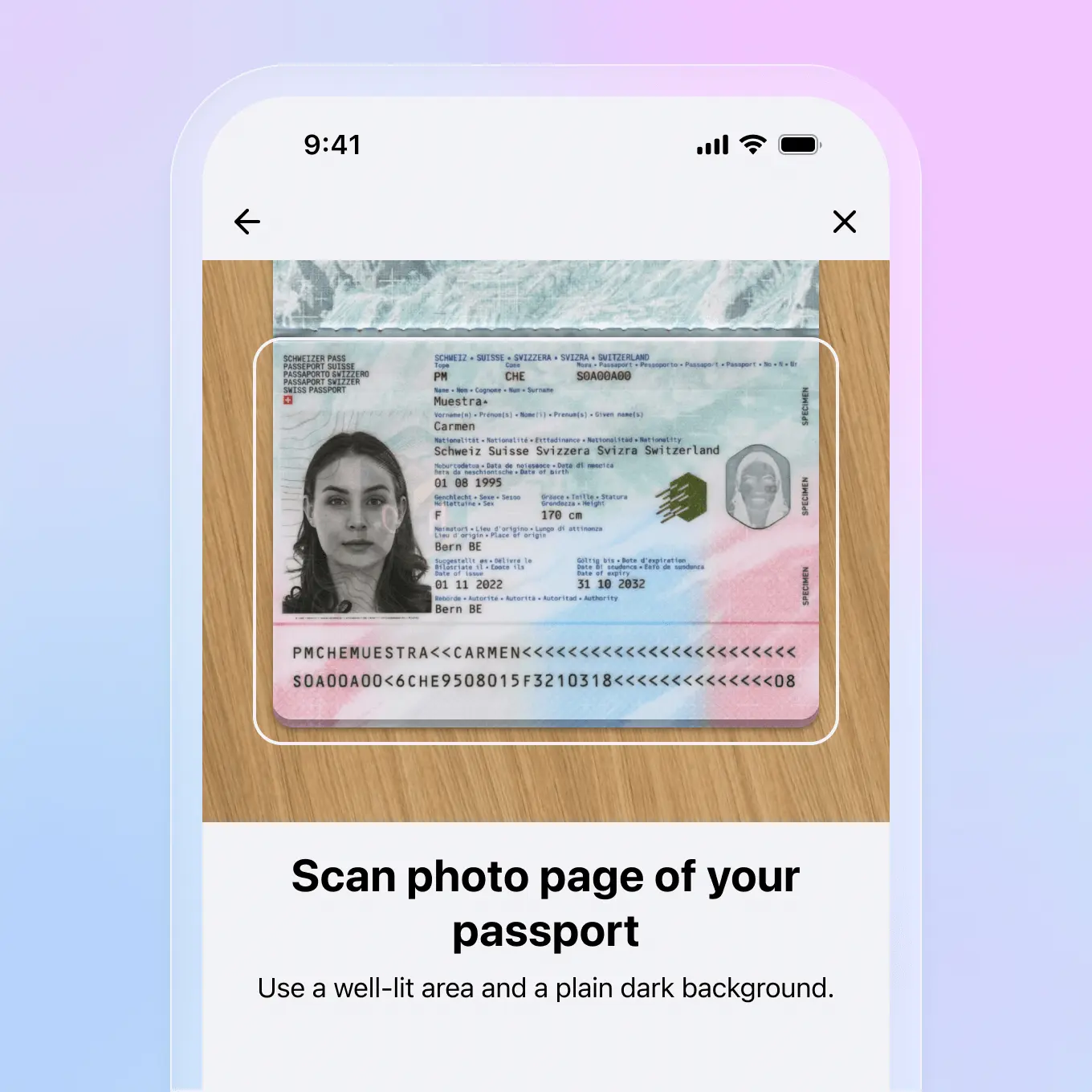

Identity document verification: Capture and authenticate government-issued ID documents. Modern systems extract data automatically and check for signs of tampering or forgery.

Biometric verification: Face matching confirms the person submitting documents matches the photo on the ID. Liveness detection prevents spoofing with photos or videos.

Address verification: Proof of address documents (utility bills, bank statements) or database checks confirm customer residence.

Database screening: Cross-reference customer information against sanctions lists, PEP databases, and adverse media sources.

Risk assessment: Score customers based on various risk factors and apply appropriate due diligence levels.

Common compliance challenges

Organizations face several recurring challenges in KYC and AML compliance:

Customer friction: Extensive verification requirements can frustrate customers and increase abandonment rates. Balancing thorough verification with smooth user experience requires careful design.

False positives: Overly sensitive monitoring systems flag too many legitimate transactions, creating review backlogs and customer complaints. Tuning detection thresholds requires ongoing attention.

International complexity: Businesses operating across borders must navigate different regulatory requirements while maintaining consistent processes.

Evolving requirements: Regulations change frequently. Staying current requires dedicated compliance resources and flexible technology platforms.

Documentation burden: Demonstrating compliance to regulators requires comprehensive documentation of policies, procedures, training, and individual verification decisions.

Technology solutions for compliance

Modern compliance platforms address many of these challenges through automation and integration:

Automated document processing: AI-powered systems capture, classify, and extract data from identity documents, reducing manual review time.

Real-time verification: Instant checks against databases and watchlists enable faster onboarding decisions.

Risk-based workflows: Adaptive processes apply appropriate verification levels based on risk assessment, streamlining low-risk cases while ensuring high-risk customers receive proper scrutiny.

Audit trails: Comprehensive logging of all verification steps and decisions supports regulatory examination.

Folio's identity verification platform supports KYC and AML compliance with configurable verification workflows, global document coverage, biometric verification, and integration with screening services. The platform generates audit-ready reports documenting verification results and decision rationale.

ID verification

Check official documents and confirm identity in more than 200 places around the world.

Effective KYC and AML compliance protects both businesses and the broader financial system from abuse. While requirements continue evolving, the fundamental goal remains constant: know your customers, understand the risks they present, and monitor for suspicious activity. Modern technology makes achieving these goals more efficient than ever, enabling businesses to meet regulatory requirements while delivering the smooth customer experiences that drive growth.

Keep reading

Best identity verification platforms in 2025

Research

Dec 19, 2025

Best identity verification platforms in 2025

Research

Dec 19, 2025

The EU is giving everyone a digital ID wallet. Here's what that means.

Product

Oct 25, 2025

The EU is giving everyone a digital ID wallet. Here's what that means.

Product

Oct 25, 2025

How NFC chip scanning verifies your passport in seconds

Business

Oct 20, 2025

How NFC chip scanning verifies your passport in seconds

Business

Oct 20, 2025